Artificial intelligence (AI) isn’t a futuristic technology anymore. It’s already used by businesses to enhance systems and processes across a range of functions. According to a McKinsey study, AI adoption in the business community has more than doubled since 2017. Popular use cases range from service operations optimisation to product enhancement, from customer acquisition and lead generation to risk modelling and analytics.

AI’s ability to analyse large amounts of data quickly and accurately allows organisations to automate repetitive tasks, streamline processes, and improve decision-making. That’s backed up by firm evidence. In 2021, 32% of businesses that adopted AI said it reduced costs by up to 20%. And 63% attributed their use of AI to a 10% boost in revenue, according to the same McKinsey study.

The finance office is uniquely positioned to capture the benefits of AI as it has access to a wealth of data from across the organisation. With that in mind, here are five ways AI can help CFOs improve the efficiency and effectiveness of the finance function.

Discover why CFO tech is so damn hot right now…

Automate financial processes

One of the most straightforward ways AI can help CFOs is by automating time-consuming and repetitive tasks, such as data entry, reconciliation and invoice processing. By using technologies such as optical character recognition (OCR) and natural language processing (NLP), AI-powered systems can quickly and accurately extract information from financial documents and enter it into the relevant systems, freeing up CFOs to focus on more strategic tasks.

A study by Accenture found that robotic process automation (RPA) and AI can automate more than 80 percent of activities involved in transaction processing, accounting, exercising control, ensuring compliance, and reporting. These activities historically consumed 50-75% of staff time.

Enhance financial planning & analysis

An EY survey found that CFOs’ number one priority for the finance function is “improving data and analytics capabilities to transform forecasting, risk management and understanding of value drivers.”

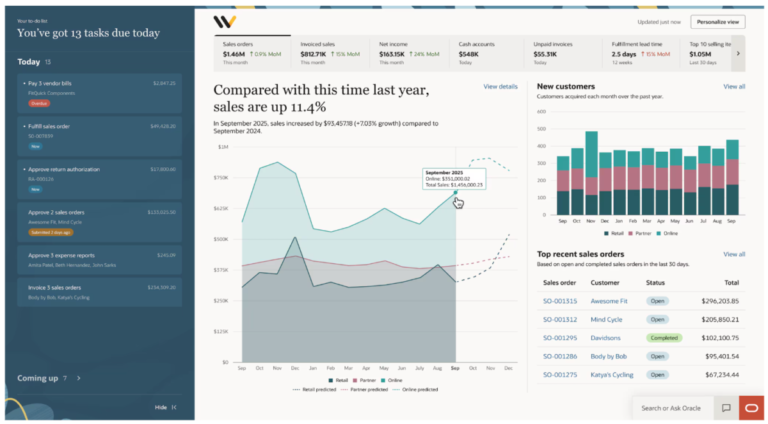

This is why finance executives are incorporating AI into financial planning and analysis (FP&A) activities. For a start, AI-powered software can automatically extract and analyse data from internal sources, such as income statements and balance sheets. But its power goes well beyond this. It can pull in data from a host of external factors, including changes in the economy, shifts in consumer demand and fluctuations in currency exchange rates.

Besides cutting down on time-consuming and labour-intensive tasks, AI-driven advanced analytics minimises human error. And it uncovers patterns and trends that may not be immediately obvious to human analysts. Ultimately, this yields valuable and timely insights that can be used to gain a more holistic view of the company’s performance – and create accurate financial models and forecasts that enable better decision-making.

Identify fraud and errors

According to a report released by PwC in 2022, 46% of organisations reported experiencing fraud, corruption or other types of financial crime in the past 24 months. Such crimes can have a significant impact on an organisation’s revenue, in some cases costing tens of millions of dollars.

It’s essential for organisations to have strong fraud detection and prevention capabilities. Thankfully, AI can help in this area too.

Machine learning (ML) algorithms can be used to monitor financial transactions in real-time; it can then identify patterns and anomalies that may indicate fraudulent or erroneous activity. Examples include identifying unusual patterns of spending and large transactions from unfamiliar vendors.

AI-powered fraud detection systems can also be trained to recognise specific signs of fraudulent activity, such as duplicate invoices or irregular payment patterns.

Identify opportunities to cut costs

By analysing data on spending patterns, production processes and supplier performance, AI can help CFOs identify potential cost savings and opportunities to improve efficiency that may not be immediately apparent.

For example, insights generated from this analysis can show which suppliers have the best prices and may help the finance department to identify areas where operational improvements could be made. By using AI, CFOs can have a clear view of their cost structure and make better-informed decisions to optimise the company’s finances.

Moreover, ML can be used to continuously monitor equipment and predict when parts will wear out or fail. This allows for maintenance work to be carried out before expensive repairs become necessary.

Streamline financial compliance

CFOs can use AI-powered solutions to automatically monitor financial transactions and ensure compliance with relevant regulations and laws. AI can identify and flag potential compliance issues, such as transactions that exceed regulatory limits or transactions with suspect vendors.

This allows finance teams to proactively mitigate compliance risk, rather than taking a passive stance. And it should mean they avoid potential fines and other penalties in the future.

Bonus: lay the data foundations first

While the potential of AI in finance is clear, its effectiveness ultimately depends on the quality of the data that feeds it. AI systems are only as reliable as the datasets they are trained on and draw from. Incomplete, inconsistent or siloed financial data will not magically become strategic insight simply because an algorithm is applied to it.

Many organisations still operate with fragmented ERP environments, legacy systems and disconnected spreadsheets across departments. In these conditions, implementing AI on top of poor data foundations can amplify errors rather than eliminate them. Duplicate records, inconsistent coding structures and outdated information will undermine even the most sophisticated machine learning models.

For CFOs, this makes data governance a strategic priority. Establishing clear data ownership, standardising definitions of key financial metrics, and investing in integrated systems are critical early steps. It may also require collaboration with IT and operations to ensure financial and operational datasets are aligned.

There is also the question of data security and access controls. As AI models increasingly process sensitive financial and customer information, organisations must ensure that robust cybersecurity measures and permission frameworks are in place.

In short, successful AI adoption in the finance function is as much about disciplined data management as it is about technology investment. CFOs who focus on building clean, structured and accessible data environments will be far better positioned to realise meaningful, scalable returns from AI initiatives.

Missed opportunity… until now

Given that the finance office is responsible for maximising profitability and driving growth in an organisation, the CFO to a large extent bears responsibility for ensuring that the organisation is reaping the benefits of AI. Yet, a recent IBM report found that AI is being under-utilised in the finance function. In fact, according to the report, the effectiveness of the finance function in control/risk management and strategy planning and execution declined between 2013 and 2021.

CFOs risk letting their organisations fall behind if they don’t begin harnessing the power of AI to streamline financial processes and maximise the effectiveness of the finance function. However, they shouldn’t rush to jump on the AI bandwagon without first ensuring they have a clear plan in place. This means weighing the benefits and limitations of AI and thinking about how to implement it in a way that helps human workers do their jobs more effectively. It must also align with the goals of the business.

Our advice? Start small and scale up gradually.

As technology continues to advance, the capabilities of AI will only expand, providing CFOs with even more opportunities to streamline their operations, improve their decision-making, and drive business growth. Forward-thinking CFOs should ensure that they stay informed of the latest developments and best practices to make the most of this technology.

This article was updated in 2026 with an additional bonus section on data readiness.